Contact Us

Two Pershing Square 2300 Main Street, Suite 170 Kansas City MO 64108Two Pershing Square

2300 Main Street, Suite 170

Kansas City, MO 64108

Directions

Telephone: (816) 221-6600

Toll Free: 1 (877) 284-6600

Fax: (816) 221-6612

In 2022, 14% of motorists, or about one in seven drivers were uninsured, according to a 2023 study by the Insurance Research Council (IRC) (in Missouri, it was 16%). While all states require drivers to carry a minimum amount of car liability insurance on a vehicle, not everyone does so you want to make sure you have enough uninsured coverage.

In Missouri, drivers are required to carry a car liability insurance to protect and compensate others injured in a car accident where you are legally at fault, and uninsured insurance (UM) to protect you from drivers who do not have car insurance.

As the name implies, uninsured motorist coverage applies when you get in an accident with a driver who does not carry any insurance. It also applies should the other driver leave before you can gather his or her insurance information (i.e., hit-and-run accident).

Uninsured motorist (UM) coverage applies if:

Again, as the name implies, underinsured motorist (UIM) coverage applies when you are injured by a driver whose coverage limits do not cover the cost of damage and injuries.

This means that the other driver’s insurance would cover expenses up to his or her policy limits. So, for instance, if the other driver’s policy limit was $25,000 and the damages and injuries incurred expenses of $50,000, you would be able to file a claim for $25,000 with that person’s insurance. After that, your UIM insurance would pay the rest, that is, up until your coverage limits have been reached.

The best advice, make sure you have adequate UM/UIM coverage in your car insurance policy.

There is a practice called “stacking.” Stacking means that you can combine insurance coverage limits to account for more than one vehicle insured on the same policy or under separate policies.

The benefit of being able to stack your UM/UIM coverage is that it raises the potential amount of coverage you can use in case of an accident with an uninsured or underinsured driver.

If your coverage is unstacked, or you only have one insured vehicle, then your level of coverage equals the limit listed on your policy.

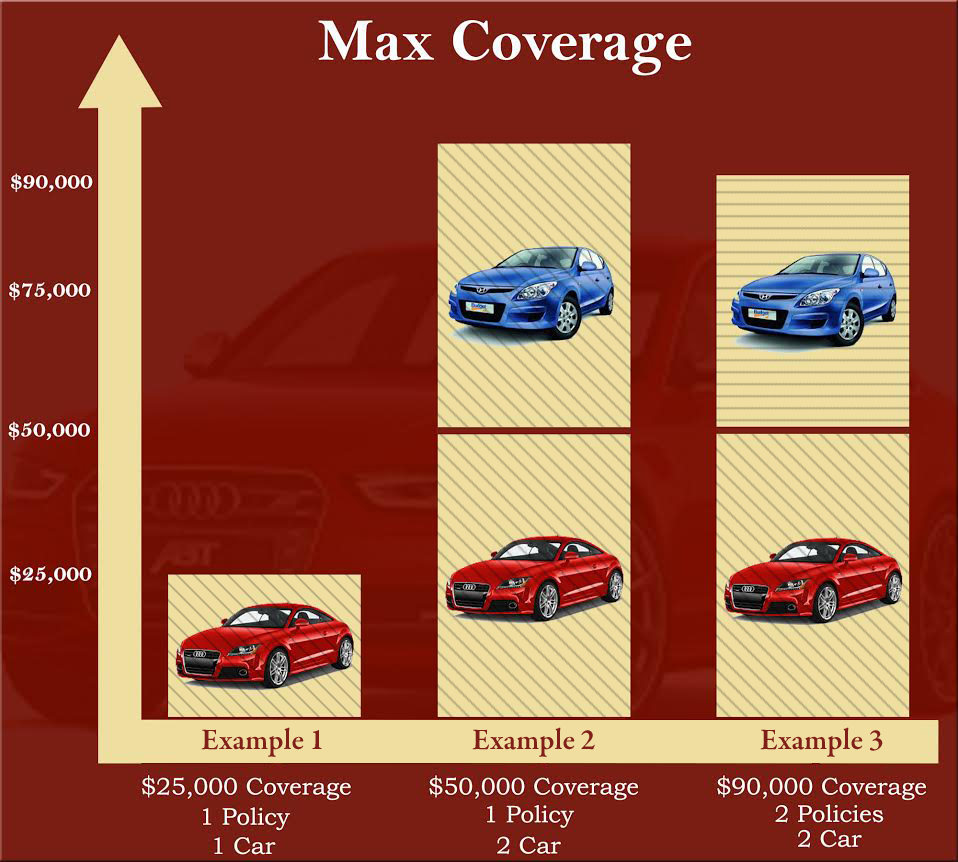

Let’s look at some examples.

Example 1: The limit on your policy is set at $25,000. In unstacked coverage, you will only receive coverage up to that maximum amount of $25,000.

Example 2: If you stack within policies, you may be able to combine the coverage limits for multiple vehicles on one policy. For instance, if you have two cars on a single car insurance policy and your UM limit was $50,000 you could potentially combine your UM coverage limits for a total of up to $100,000.

Example 3: If you stack across policies, meaning that your two vehicles are on two separate policies, and your UM limit was $40,000, you could potentially file a claim using both policies up to $80,000.

When insuring your vehicles, talk with your insurance agent about the benefits of stacked vs. unstacked UM/UIM coverage.

When you have been in an accident with an uninsured or underinsured drive, your personal injury attorney can help you determine if you are able to stack.

In accidents where the other driver is uninsured or underinsured, it can be confusing trying to figure out what his or her insurance will cover and what yours will cover. If you are unaware of stacking, you could also lose out on a considerable amount of money to cover your expenses.

In accidents where the other driver is uninsured or underinsured, it can be confusing trying to figure out what his or her insurance will cover and what yours will cover. If you are unaware of stacking, you could also lose out on a considerable amount of money to cover your expenses.

Before you discuss your claim with an insurance adjuster, make a statement, sign any forms or accept a settlement offer, contact the law offices of Nash & Franciskato at (877) 284-6600. One of our experienced staff will speak with you personally and will provide you with a free, no-obligation review of your case.

Would you like to receive news and blog updates regularly? Sign up to receive our email newsletter. Your email address will only be used to send you our newsletter and respond to inquiries.

Past results afford no guarantee of future results and each case is different and is judged on its own merits. The choice of a lawyer is an important decision and should not be based solely upon advertisements.

Editor’s Note: This post was originally published November 16, 2015. It was reviewed on March 8, 2024, updated for content and accuracy and re-published on March 9, 2024.